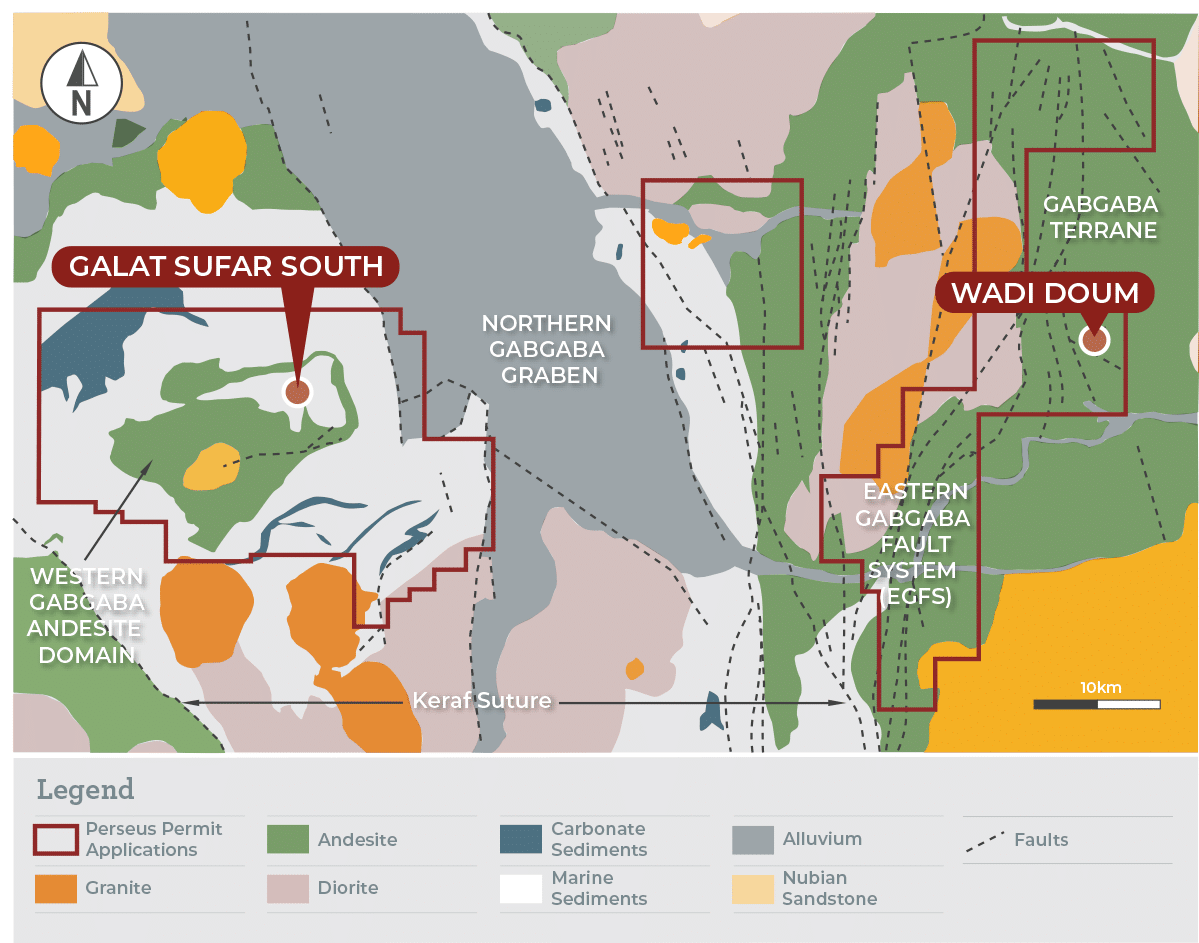

3.34 million oz/gold

M&I RESOURCES*

2.85 million oz/gold

P&P Reserves*

2012

Joint venture agreement signed with Meyas Nub, Orca holding 70% interest Galat Sufar South (GSS) deposit discovered Exploration drilling campaign kicked off by Orca to refine understanding of resource and reserves

2014

Maiden Resource reported for GSS

2015

Updated Resource incorporating the Wadi Doum deposit

2016

Preliminary economic assessment published

2017

Water resource discovered

2018

Block 14 Feasibility Study released by Orca

2020

Feasibility Study Revised by Orca

2022

Perseus Acquisition of Orca Gold and the Block 14 Project Future

2022

Pre-commitment funding for drilling to further firm up resource and assist in finalising study

2023

Preparation of FEED study for final investment decision